Understanding the Mortgage System

Introductory Overview on Mortgage Systems Each and Every Detail Filled Out

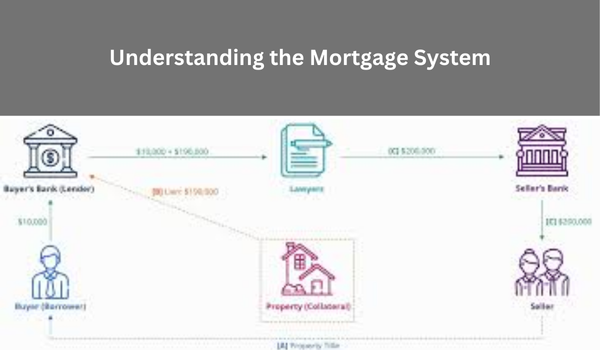

Obtaining a mortgage is perhaps one of the most important steps you take in buying a house. With this particular financial tool, people are able to purchase property without having to pay the whole amount up front. Instead, payment will be paid by either a bank or other financial institution and then paid back over the course of several decades. But you may be wondering, how does the whole mortgage system work? What other types of mortgage tools are available for individuals? This particular guide takes an in-depth look at how mortgages work, how you can receive them and other commonly asked questions regarding mortgages.

The Guide For Getting the Best Mortgages In 2025

1. What Exactly Is A Mortgage?

Mortgages can be defined as loans which are specifically utilized to carry out real estate purchases. The word “mortgage” comes from the contract which is signed between a lender like a bank and the borrower. In such an agreement, the borrower gets permission to receive the loan amount under the terms that the amount will be repaid with interest over a certain period. If the borrower is not able to follow through on the repayment terms, then the lender has the right to take over the property through a legal process known as foreclosure.

For most people, the repayment term of mortgages is generally between 15 to 30 years, however, there may be other terms available as well.

Mortgage payments usually consist of two elements: principal and interest. The original loan taken is referred to as the principal, whereas the cost involved in borrowing that amount is termed as interest.

2. Types of Mortgages

There are different types of mortgages catering to various financial needs. Some of the most popular types of mortgages are:

Fixed-Rate Mortgage

Fixed-rate mortgages are a type of mortgage in which the interest rate does not vary for the entirety of the loan repayment duration. Thus, the borrower’s monthly payments tend to be constant, which is advantageous for homeowners looking to plan their budgets for the long term. The popularity of fixed-rate mortgages can be attributed to their provision of economic stability and predictability.

Adjustable-Rate Mortgage (ARM)

Adjustable-rate mortgage (ART) is said to have an interest rate which can change over the term of the loan due to fluctuations in the market. A lower interest rate is commonly attached for an initial period of time which is then periodically adjusted based on a particular index. An adjustable-rate mortgage usually offers lower interest rates in the beginning but they come with a higher risk as the rates may change in the future, leading to increased monthly payments.

Interest-Only Mortgage

Borrowers make interest-only payments for a certain time period, usually 5 to 10 years. After that period, the borrower must start repaying both the principal loan amount and interest, which can lead to a significant increase in monthly payment amounts.

This type of mortgage is used by borrowers who either expect a raise or wish to sell a property before the interest only period expires.

Federal Housing Administration (FHA) Loan

These loans are backed by the government with an intention to support low to medium-income earners get a house. It is easy to qualify for an FHA loan as the credit scores needed are lower than that of mortgages. The down payment is usually lower, around 3.5% and first-time home buyers usually prefer FHA loans.

Veterans Affairs (VA) Loan

These loans are issued to enables armed forces veterans, active duty, and their families. They are Underwritten by the US Department of Veteran Affairs and normally do not need down payment or PMI. VA loans also attract better offers like low rates of interest and lower closing costs.

Jumbo Loan

Jumbo loans are a type of mortgage loan classified as non-conforming because they exceed the maximum limit set by the Federal Housing Finance Agency (FHFA). Because these loans are considered higher-risk, they often come with higher interest rates and stricter eligibility criteria. Jumbo loans are used for purchasing properties that are priced above the limit for conventional loans.

Reverse Mortgage

A reverse mortgage works similarly to a regular mortgage but is specifically catered towards individuals 62 years or older. Home equity can be converted into cash. These loans benefit the mortgagor in a way as they do not require any monthly payments, rather the loan amount keeps compounding through interest, causing the client to only pay after the house is sold. These types of loans are predominantly used as a source of income during retirement.

Mortgage Process

A first time homebuyer needs to fully understand the processes necessary to obtain a mortgage. The steps to take to obtain a mortgage are outlined below: First, we need to receive lender pre-approval. This is achieved by filling out a simple application form. The form has a few fields such as credit score, net income, and other debts. The lender will use the information to ascertain the loan amount and the rate of interest offered. Pre-approval simplifies budgeting for the loan and actual home purchase. Getting a pre-approval is faster than going through the mortgage application process that follows the purchase agreement. The buyer is strongly advised to pursue a pre-approval. And the second step would be to start a search for a property that matches your budget. Most buyers will hire a real estate agent to assist them with finding homes fitting their budgets and requirements.

Mortgage Documentation Step 3

After choosing a preferred home, it is now time to apply for a mortgage. It is necessary to submit an application encompassing specifics of your financial situation, which will help the lender determine your eligibility to repay the loan. For this step, tax returns, bank account statements, and employment proof will be needed.

Loan Offer and Approval Step 4

Upon getting approved for a mortgage, the lender will send an offer containing terms and conditions of the loan such as the loan amount, repayment period, and interest fee. A written offer is sent awaiting your consent, later on, shall undergo the other stages of the process.

Closing Step 5

In this step, funding, and signing all legal documents, such as the title and mortgage agreement, and paying for assessments, inspections and legal fees will take place giving you full ownership.

Top Ten Tips for CPA Mortgage Loan Success

Essential Mortgage Terminology 4

Familiarity with some more terms that relate to mortgages can aid you throughout the process:

Principal: This is an initial sum of loan that a user opts to take.

Interest Rate: Due on the amount lent out, this is the percentage that the borrower is liable to pay as interest over a predefined period.

Down Payment: This is the first installment that a buyer pays toward the purchase price of the property. The down payment is usually 3% to 20% of the selling price.

PMI (Private Mortgage Insurance): Insurance taken by the lender which covers them if the borrower defaults on the loan. If the borrower is putting down less than 20% of the mortgage, PMI is usually a requirement.

Escrow: Account that holds funds for property taxes, insurance, and other related costs incurred for the loan. The account is managed by a neutral intermediary.

Amortization: The gradual reduction of the loan balance by the constant repayment of the principal.

Foreclosure: It is the legal exercise of the right of a mortgage lender to sell the mortgaged property after the borrower defaults during the period of the loan.

Frequently Asked Questions (FAQ) Understanding the Mortgage System

What credit score do I need to qualify for a mortgage?

For a conventional loan, one normally needs a credit score that exceeds 620. However, with loans that are backed by the government, such as FHA and VA loans, the regulations are less strict and thus the credit score requirements are lower.

A better credit rating makes it easier to acquire loans, since financial institutions tend to offer lower rates of interest to those with credit ratings above average.

How large should my down payment be? You should aim to save between 3%-20% of the value of the property.

The minimum amount necessary to make the down payment varies depending on the specific loan being sought. A normal or conventional loan would require at a minimum a 5% down payment, with 20% being preferable to avoid PMI. FHA loans even allow a minimum of 3.5% set aside for the down payment, and in some instances, no down payment is necessary for certain VA loans.

What if my score is below average, do I still qualify for a mortgage?

Securing a mortgage with a weak credit rating is entirely plausible, only that it is a tedious task with the guarantee of facing greater obstacles such as not so favorable rates. Loans which are backed up by the government like FHA loans are aimed at borrowers who tend to have a lower credit score.

Interest rate vs APR, how do they differ?

When a loan is taken out, there are terms and lending conditions that need to be met. One of them includes a calculated value on top of the principal that is needed to be paid back after a specified amount of time called interest rate which is usually in the form of a yearly percentage. In comparison to an interest rate, APR or Annual Percentage Rate takes into account the interest rate and additional fees related to the loan.

What precisely is a penalty for prepayment?

A prepayment penalty is a fee some mortgage lenders impose if you decide to pay off your mortgage before it is due. There are not all mortgages that have prepayment penalties, they have less prevalence nowadays than before. Remember to always look at the fine print and the terms of the mortgage before you affix your signature.

By taking the time to understand the different types of mortgages, the application process involved, as well as relevant concepts, you will be in a better position to make decisions. Buying a home for the first time or refinancing, you will need to understand these things. These things will come in handy if you want to get the best mortgage terms suitable for your situation.